Do You Need Key Person Insurance?

Do You Need Key Person Insurance? Protecting Your Business from the Unexpected

What Would Happen If Your Business Lost Its Most Important Person?

Every business has at least one individual whose expertise, leadership, or client relationships are essential to operations. This could be the founder, a top executive, or a key employee with specialized knowledge. But what happens if that person suddenly passes away or becomes incapacitated?

For many small businesses, losing a key person can create financial instability, lost revenue, and even business failure. That’s where Key Person Insurance comes in.

In this blog, we’ll explain how Key Person Insurance works, who needs it, and why it’s a crucial safeguard for protecting your business from unexpected losses.

What Is Key Person Insurance?

Key Person Insurance is a life and disability insurance policy that a business takes out on an essential employee. The business is both the policyholder and the beneficiary, meaning if the insured person dies or becomes disabled, the company receives a payout.

This payout helps cover the financial impact of losing a key person, including:

- Recruiting and training a replacement

- Offsetting lost revenue

- Covering outstanding debts or obligations

- Maintaining business stability during the transition

In essence, Key Person Insurance is a financial safety net that allows businesses to recover and continue operations.

Who Needs Key Person Insurance?

Not every employee requires Key Person Insurance, but if losing an individual would significantly impact the company's ability to operate, they should be covered. This often includes:

✅ Business Owners & Founders – If you own the business, your sudden absence could lead to financial instability, making this coverage essential.

✅ Executives & Decision-Makers – CEOs, CFOs, and other leadership team members often drive strategic decisions that impact long-term business success.

✅ Top Salespeople or Client-Facing Roles – If a specific employee is responsible for a large percentage of revenue or maintains critical client relationships, their absence could mean major financial losses.

✅ Specialized Employees – If your company relies on one person’s unique skills, such as a lead engineer, designer, or scientist, their loss could cause serious disruption.

What Does Key Person Insurance Cover?

A Key Person Insurance policy typically provides:

🔹 Death Benefit – If the insured person passes away, the business receives a lump sum payout.

🔹 Disability Coverage (Optional Add-On) – If the key employee becomes permanently disabled and can no longer work, the business may receive compensation.

🔹 Business Continuity Support – The funds can be used to cover operational costs, pay debts, or keep the business running while a replacement is found.

🔹 Buyout Protection (For Partnerships) – In businesses with multiple owners, Key Person Insurance can help fund a buyout agreement, ensuring the business remains operational if one partner passes away.

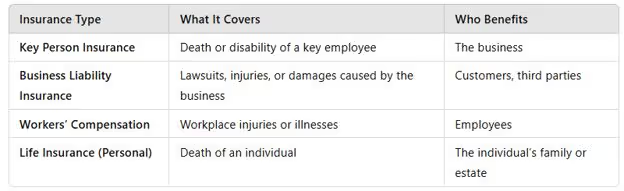

Key Person Insurance vs. Other Business Insurance

Many business owners assume that traditional business liability insurance or workers’ compensation insurance will cover these situations, but that’s not the case. Here’s how they differ:

Key Person Insurance is specifically designed to protect the business itself, rather than individual employees or third parties.

What Happens If You Don't Have Key Person Insurance?

Without Key Person Insurance, businesses often struggle to stay afloat after losing an essential employee. Some of the biggest risks include:

🚨 Financial Strain– Losing a key employee may result in lost clients, delayed projects, or a decrease in revenue.

🚨 Business Closure– If the key person is also the business owner, the company may lack the funds to continue operations.

🚨 Forced Liquidation– The company may be forced to sell assets or take on debt to cover expenses.

🚨 Loss of Investor or Lender Confidence – Investors and lenders may see the business as too risky without a plan in place.

For many small businesses and startups, a single loss can be catastrophic—which is why Key Person Insurance is often an essential part of business risk management.

How Much Key Person Insurance Do You Need?

The amount of coverage depends on how much financial impact losing that person would have on the business. Consider the following:

📌 Revenue Contribution– How much revenue does this person generate directly or indirectly?

📌 Replacement Costs– How much would it cost to recruit, train, and onboard a replacement?

📌 Debt Obligations– Will the business struggle to meet loan payments if this person is gone?

📌 Time to Recover– How long would it take for the business to stabilize after their departure?

A general rule of thumb is to insure a key employee for 5-10 times their annual salary, but consulting with a financial advisor can help determine the right amount.

Final Thoughts

Key Person Insurance isn’t just for large corporations—it’s a critical tool for small businesses and startups that depend on a few key individuals. Having this coverage ensures that if the unexpected happens, your business has the financial support to navigate the transition and continue operations.

If you’re unsure whether your business needs Key Person Insurance, now is the time to evaluate your risk. Schedule a consultation today to discuss your business’s unique needs and ensure you’re protected for the future

This article is a service of Dolev Law, a Personal Family Lawyer® Firm. We don’t just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love. That's why we offer a Life & Legacy Planning Session™, during which you will get more financially organized than you’ve ever been before and make all the best choices for the people you love. You can begin by calling our office today to schedule a Life & Legacy Planning Session™.

Disclaimer

The information provided in this blog is intended for general informational purposes only and does not constitute legal advice. Overtime pay laws, salary thresholds, and other employment regulations are subject to change, and their application can vary depending on specific circumstances and jurisdictions. We recommend consulting with a qualified attorney or human resources professional to address your specific legal needs or compliance questions. This blog should not be relied upon as a substitute for personalized legal advice. Reading this blog or contacting our firm does not establish an attorney-client relationship. If you need assistance with employment law compliance or other legal matters, feel free to reach out to us to discuss your specific situation.

%2520(34).avif)

%2520(33).avif)

%2520(29).avif)